Accrued Expenses

An adjusting entry to accrue expenses is necessary when there are

unrecorded expenses and liabilities that apply to a given accounting

period. These expenses may include wages for work performed in the

current accounting period but not paid until the following accounting

period and also the accumulation of interest on notes payable and other

debts.

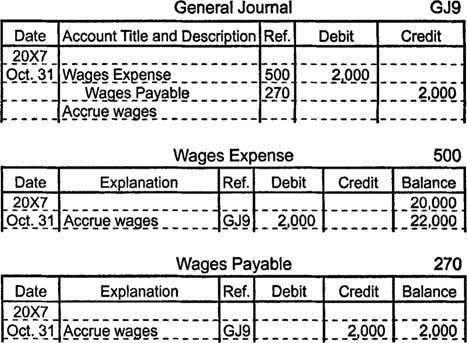

Suppose a company owes its employees $2,000 in unpaid wages at the

end of an accounting period. The company makes an adjusting entry to

accrue the expense by increasing (debiting) wages expense for $2,000 and

by increasing (crediting) wages payable for $2,000.

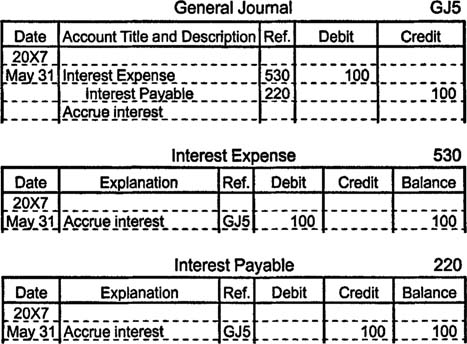

If a long-term note payable of $10,000 carries an annual interest

rate of 12%, then $1,200 in interest expense accrues each year. At the

close of each month, therefore, the company makes an adjusting entry to

increase (debit) interest expense for $100 and to increase (credit)

interest payable for $100.

Accounting records that do not include adjusting entries for

accrued expenses understate total liabilities and total expenses and

overstate net income.

Tidak ada komentar:

Posting Komentar