Journal Entries

Tracking business activity with T accounts would be cumbersome

because most businesses have a large number of transactions each day.

These transactions are initially recorded on

source documents, such as invoices or checks. The

first step in the accounting process is to analyze each transaction and

identify what effect it has on the accounts. After making this

determination, an accountant enters the transactions in chronological

order into a journal, a process called

journalizing the transactions. Although many companies use specialized journals for certain transactions, all businesses use a

general journal. In this book, the terms

general journal and

journal are used interchangeably.

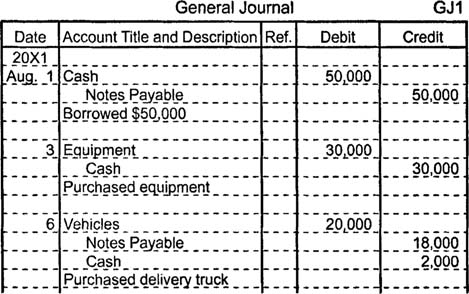

The journal's page number appears near the upper right corner. In

the example below, GJ1 stands for page 1 of the general journal. Many

general journals have five columns: Date, Account Title and Description,

Posting Reference, Debit, and Credit.

To record a

journal entry, begin by entering the date of the

transaction in the journal's date column. For convenience, include the

year and month only at the top of each page and next to each month's

first entry. In the next column, list each account affected by the

transaction on a separate line, and enter a short description of the

transaction immediately below the list of accounts. The accounts being

debited always appear above the accounts being credited, which are

indented slightly. The posting reference column remains blank until the

journal entry is transferred to the accounts, a process called

posting, at which time the account's number is

placed in this column. Finally, enter the debit or credit amount for

each account in the appropriate columns on the right side of the

journal. Generally, one blank line separates each transaction.

Tidak ada komentar:

Posting Komentar