Unearned Revenues

Unearned revenues are payments for future services

to be performed or goods to be delivered. Advance customer payments for

newspaper subscriptions or extended warranties are unearned revenues at

the time of sale. At the end of each accounting period, adjusting

entries must be made to recognize the portion of unearned revenues that

have been earned during the period.

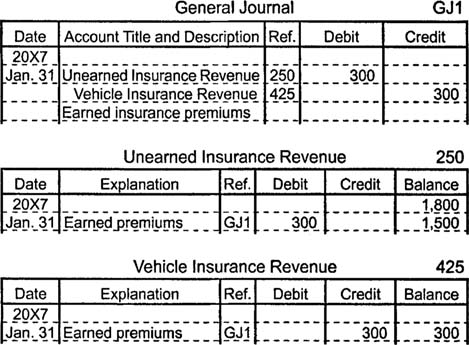

Suppose a customer pays $1,800 for an insurance policy to protect

her delivery vehicles for six months. Initially, the insurance company

records this transaction by increasing an asset account (cash) with a

debit and by increasing a liability account (unearned revenue) with a

credit. After one month, the insurance company makes an adjusting entry

to decrease (debit) unearned revenue and to increase (credit) revenue by

an amount equal to one sixth of the initial payment.

Accounting records that do not include adjusting entries to show

the earning of previously unearned revenues overstate total liabilities

and understate total

Prepaid Expenses

Prepaid expenses are assets that become expenses as

they expire or get used up. For example, office supplies are considered

an asset until they are used in the course of doing business, at which

time they become an expense. At the end of each accounting period,

adjusting entries are necessary to recognize the portion of prepaid

expenses that have become actual expenses through use or the passage of

time.

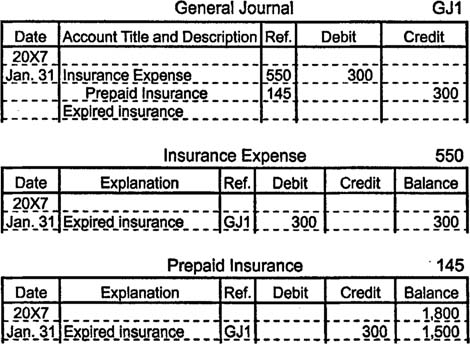

Consider the previous example from the point of view of the

customer who pays $1,800 for six months of insurance coverage.

Initially, she records the transaction by increasing one asset account

(prepaid insurance) with a debit and by decreasing another asset account

(cash) with a credit. After one month, she makes an adjusting entry to

increase (debit) insurance expense for $300 and to decrease (credit)

prepaid insurance for $300.

Prepaid expenses in one company's accounting records are often—but

not always—unearned revenues in another company's accounting records.

Office supplies provide an example of a prepaid expense that does not

appear on another company's books as unearned revenue.

Accounting records that do not include adjusting entries to show

the expiration or consumption of prepaid expenses overstate assets and

net income and understate expenses.

Tidak ada komentar:

Posting Komentar