Adjusting

Entries

Before financial statements are

prepared, additional journal entries, called adjusting entries, are made

to ensure that the company's financial records adhere to the revenue

recognition and matching principles. Adjusting entries are necessary because a

single transaction may affect revenues or expenses in more than one accounting

period and also because all transactions have not necessarily been documented

during the period.

Each adjusting entry usually affects

one income statement account (a revenue or expense account) and one balance

sheet account (an asset or liability account). For example, suppose a company

has a $1,000 debit balance in its supplies account at the end of a month, but a

count of supplies on hand finds only $300 of them remaining. Since supplies

worth $700 have been used up, the supplies account requires a $700 adjustment

so assets are not overstated, and the supplies expense account requires a $700

adjustment so expenses are not understated.

Adjustments fall into one of five

categories: accrued revenues, accrued expenses, unearned revenues, prepaid

expenses, and depreciation.

Accrued Revenues

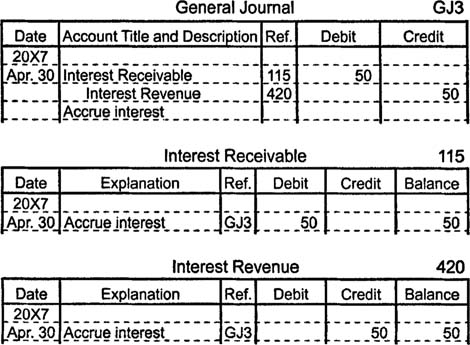

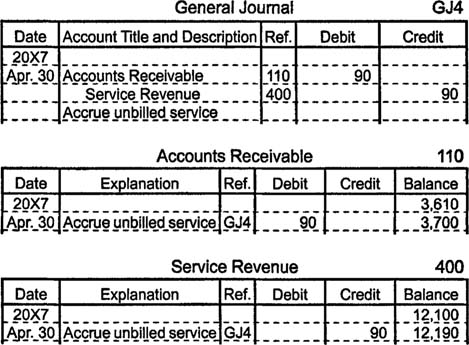

An adjusting entry to accrue revenues is necessary when revenues have been earned but not yet recorded. Examples of unrecorded revenues may involve interest revenue and completed services or delivered goods that, for any number of reasons, have not been billed to customers. Suppose a customer owes 6% interest on a three-year, $10,000 note receivable but has not yet made any payments. At the end of each accounting period, the company recognizes the interest revenue that has accrued on this long-term receivable.

|

Most textbooks use a 360-day year for interest calculations, which is done here. In practice, however, most lenders make more precise calculations by using a 365-day year.

Since the company accrues $50 in interest revenue during the month, an adjusting entry is made to increase (debit) an asset account (interest receivable) by $50 and to increase (credit) a revenue account (interest revenue) by $50.

|

|

|

|

|

|

|

|

|

|

Tidak ada komentar:

Posting Komentar